DMT vs PTA Process Economics Market Hit USD 14.38 Billion by 2034 at 5.8% CAGR

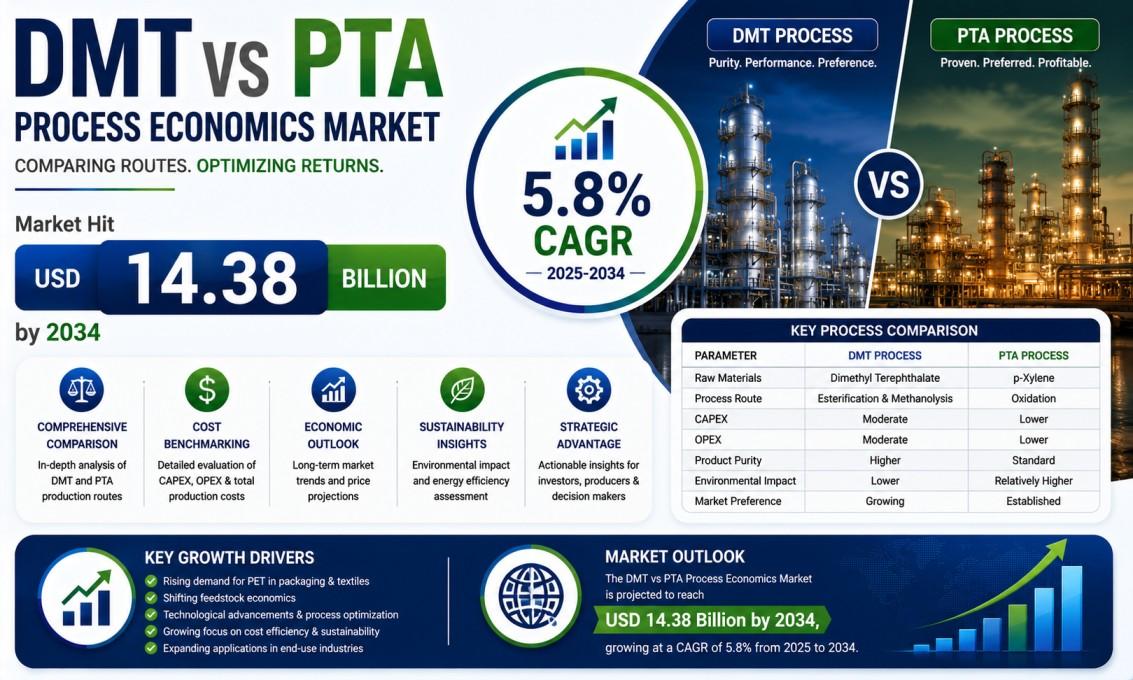

Global Dimethyl Terephthalate (DMT) vs Purified Terephthalic Acid (PTA) Process Economics Share market was valued at USD 8.74 billion in 2025 and is projected to reach USD 14.38 billion by 2034, exhibiting a remarkable CAGR of 5.8% during the forecast period.

Dimethyl Terephthalate (DMT) and Purified Terephthalic Acid (PTA) serve as the two principal intermediates in the production of polyethylene terephthalate (PET) and polyester fibers, forming the foundational feedstock for downstream applications in textiles, packaging, and industrial materials. While both routes rely on para-xylene as the primary raw material, they diverge markedly in process technology, capital requirements, operating costs, and compatibility with modern polymerization systems.

Get Full Report Here: https://www.24chemicalresearch.com/reports/310538/dimethyl-terephthalate-dmt-vs-pta-process-economics-share-market

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities.

Powerful Market Drivers Propelling Expansion

-

Sustained Demand for Polyester Intermediates Anchoring DMT and PTA Process Relevance: The global polyester value chain remains one of the most structurally vital segments of the petrochemical industry. Both DMT and PTA function as essential precursors to PET resin, polyester fiber, and film. While PTA has captured the dominant share of global terephthalate capacity, especially across Asia, DMT continues to hold meaningful relevance in specific regional markets and specialized applications.

-

Capital Cost Differentials and Feedstock Economics Driving PTA Process Adoption: The most decisive factor influencing the competitive landscape is the significant difference in process economics at commercial scale. PTA production through the Amoco oxidation process, using p-xylene feedstock and acetic acid solvent, achieves notably lower variable costs per metric ton in plants exceeding 500,000 tonnes per annum. Mega-scale PTA facilities in China, India, and Southeast Asia benefit from deep integration with paraxylene units, which further reduces feedstock costs.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/310538/dimethyl-terephthalate-dmt-vs-pta-process-economics-share-market

Significant Market Restraints Challenging Adoption

Despite its promise, the market faces hurdles that must be overcome to achieve universal adoption.

-

Structural Overcapacity in PTA and Its Cascading Pressure on Process Economics: The persistent overcapacity in global PTA production, heavily concentrated in China, represents the foremost challenge. Extensive capacity builds have at times pushed utilization rates below sustainable levels, compressing margins throughout the value chain. Smaller-scale DMT producers, operating with thinner margins, face intense downstream pricing pressure from surplus PTA, which makes continued operation difficult outside of captive or specialty contexts.

-

Technology Transition Costs and Asset Stranding Risks for DMT Operators: Legacy DMT facilities encounter substantial obstacles in an industry standardized around PTA. Converting a DMT-based complex to PTA compatibility demands major capital outlays for reactor modifications, infrastructure changes, and purification upgrades. This creates a difficult strategic choice between sustaining an uncompetitive asset or investing heavily in conversion, both challenging amid narrow industry margins.

Critical Market Challenges Requiring Innovation

The transition from laboratory success to industrial-scale manufacturing presents its own set of challenges. Maintaining consistent quality across varying production volumes remains difficult for DMT operations, while ensuring compatibility with modern downstream systems adds complexity. These technical issues require ongoing investment, creating elevated barriers for smaller participants. Additionally, the market deals with feedstock sensitivities. DMT production is notably exposed to methanol price volatility in addition to shared p-xylene costs, introducing greater economic uncertainty compared to PTA routes.

Vast Market Opportunities on the Horizon

-

Chemical Recycling of PET Creating a Renewed Role for DMT as a Recovered Intermediate: The rapid advancement of chemical recycling infrastructure for post-consumer PET opens a promising new avenue for DMT. Methanolysis processes that depolymerize PET to recover DMT and ethylene glycol are gaining commercial momentum as companies pursue closed-loop solutions.

-

Specialty Polyester and Engineering Polymer Markets Offering Differentiated Value Capture for DMT: DMT retains strong potential in segments such as polybutylene terephthalate (PBT), polytrimethylene terephthalate (PTT), and specialized copolyesters. These applications value DMT’s ester functionality for processing advantages, particularly in automotive, electrical, and electronics components. Growth in electric vehicle and high-performance materials sectors supports sustained demand insulated from bulk commodity competition.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into Purified Terephthalic Acid (PTA) Process and Dimethyl Terephthalate (DMT) Process. Purified Terephthalic Acid (PTA) Process currently leads the market, favored for its superior feedstock efficiency, lower energy use per unit, and seamless integration with large-scale polyester manufacturing. The DMT Process, while more legacy-oriented in mature markets, maintains strategic importance in regions with favorable methanol economics and in specialty applications requiring high-purity ester intermediates.

By Application:

Application segments include Polyethylene Terephthalate (PET) Production, Polybutylene Terephthalate (PBT) Production, Polytrimethylene Terephthalate (PTT) Production, and others. The PET Production segment currently dominates, driven by massive demand for packaging, beverage bottles, and textile fibers. The PTA route holds clear advantages here due to process compatibility. However, PBT and PTT segments are expected to exhibit strong relevance for DMT chemistry in engineering and specialty fiber applications.

By End-User Industry:

The end-user landscape includes Textile and Apparel Industry, Packaging Industry, Automotive and Electronics Industry, and others. The Textile and Apparel industry accounts for the major share, relying predominantly on PTA-derived materials for cost efficiency in fiber production. The Packaging and Automotive/Electronics sectors are key areas where both routes contribute, with DMT supporting high-performance engineering needs.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/310538/dimethyl-terephthalate-dmt-vs-pta-process-economics-share-market

Competitive Landscape:

The global Dimethyl Terephthalate (DMT) vs PTA process economics share market is semi-consolidated and characterized by intense competition and rapid innovation. The top three companies—Indorama Ventures Public Company Limited, Hengli Petrochemical, and Reliance Industries Limited—collectively command approximately significant share of the market as of recent years. Their dominance is underpinned by extensive production capabilities, vertical integration, and established global distribution networks.

List of Key Dimethyl Terephthalate DMT & PTA Companies Profiled:

-

Indorama Ventures Public Company Limited (Thailand)

-

Eastman Chemical Company (United States)

-

Hengli Petrochemical Co., Ltd. (China)

-

Xinfengming Group Co., Ltd. (China)

-

Rongsheng Petrochemical Co., Ltd. (China)

-

INEOS Group Holdings S.A. (United Kingdom / Switzerland)

-

Mitsubishi Chemical Corporation (Japan)

-

SABIC (Saudi Arabia)

-

Lotte Chemical Corporation (South Korea)

-

Reliance Industries Limited (India)

The competitive strategy is overwhelmingly focused on R&D to enhance process efficiency and reduce costs, alongside forming strategic vertical partnerships with end-user companies to co-develop and validate new applications, thereby securing future demand.

Regional Analysis: A Global Footprint with Distinct Leaders

-

Asia-Pacific: Stands as the dominant region in the global DMT versus PTA landscape, driven by its enormous polyester and PET manufacturing base, particularly in China, India, South Korea, and Taiwan. The region has shifted decisively toward PTA due to its cost efficiencies at scale. China accounts for the lion’s share of global PTA capacity through integrated complexes. DMT persists in select legacy and specialty roles, but new investments overwhelmingly favor PTA.

-

North America & Europe: Represent mature markets with a historical presence of DMT assets that have gradually transitioned or rationalized in favor of PTA. Legacy DMT operations continue in niche specialty segments. Both regions emphasize sustainability and circular recycling pathways, where DMT recovery from methanolysis gains attention. Higher energy and regulatory costs influence process optimization decisions.

Get Full Report Here: https://www.24chemicalresearch.com/reports/310538/dimethyl-terephthalate-dmt-vs-pta-process-economics-share-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

-

Plant-level capacity tracking

-

Real-time price monitoring

-

Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/