Aircraft Seating Market Size, Share & Growth Forecast 2025–2035

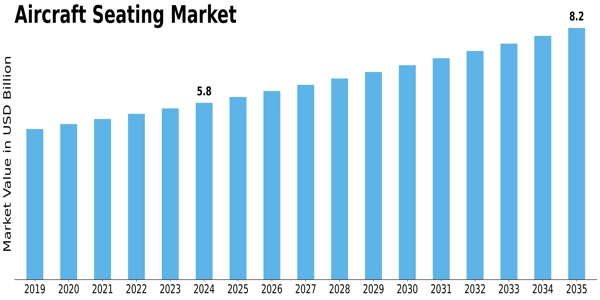

In today’s aviation landscape, comfort and efficiency are no longer mutually exclusive. The global aircraft seating market is undergoing steady expansion, driven by increasing air travel demand, evolving airline fleets and a rising emphasis on passenger experience. According to a recent study by a market-research firm, the market size was estimated at around USD 5.57 billion in 2023 and is projected to grow to approximately USD 8.2 billion by 2035, corresponding to a compound annual growth rate (CAGR) of about 3.26% during the 2025-2035 period.

Industry Overview

The aircraft seating sector lies at the intersection of aerospace manufacturing, interior design, materials engineering and regulatory compliance. Airlines are actively revamping their cabin interiors to attract passengers, reduce weight, improve fuel efficiency and meet sustainability targets. Meanwhile, seat-manufacturers must navigate stringent safety standards, ergonomic demands and cost pressures. As commercial aviation recovers and expands, the need for new seats—especially for narrow-body and regional fleets—remains robust.

Market Outlook

Looking ahead, the market is expected to continue its moderate but sustained growth. Key drivers include rising global air passenger numbers, growth of low-cost carriers, fleet modernisation and a shift toward premium economy classes. At the same time, constraints such as fluctuating material costs and regulatory certification burdens remain. The push for lighter seating materials and the integration of smart‐features offer sizeable opportunities.

Key Players’ Role

Major manufacturers and suppliers are playing a critical role in shaping the market. Firms such as Sichuan Tengdun Seating Company, Universal Aviation Seating, Recaro Aircraft Seating, Zodiac Aerospace and Thompson Aero Seating are well-positioned with strong R&D, global supply chains and partnerships with airlines and airframers. For example, some manufacturers are innovating in modular designs, connectivity-enabled seats and sustainable material use. These companies also engage in acquisitions and collaborations to broaden their portfolios and respond quickly to airline needs.

Segmentation Growth

The market can be broken down by several dimensions. By seat type, economy class dominates due to the sheer volume of seats required; this segment is projected to grow from around USD 2.88 billion in 2024 to USD 4.05 billion by 2035. Business class and first-class segments also show growth, albeit from smaller bases. By material, key categories include leather, fabric, plastic and metal. Lightweight plastics and advanced composites are gaining traction because of their role in reducing aircraft weight and fuel consumption. In terms of aircraft type, narrow-body aircraft seating constitutes the bulk of demand, given the prevalence of short- and medium-haul flights globally. Regional aircraft and wide-body segments contribute meaningfully as well. Geographically, North America holds a leading share, followed by Europe and Asia-Pacific; emerging regions like South America and the Middle East/Africa are expected to pick up momentum as air transport infrastructure expands.

Closing Thoughts

As airlines continue investing in cabin upgrades and passengers demand enhanced comfort, the aircraft seating market stands at an inflection point. Success will go to the manufacturers that can combine weight-efficient designs, comfort innovations and compliance with evolving regulatory norms. For airline operators and investors alike, this segment offers consistent growth potential—especially if aligned with sustainability and digitalisation trends.